M & M Tax Service, LLC

Professional Tax Preparation

More Knowledge = Less Taxes

About Me

My name is Michael Reed, and I’ve been in the tax preparation field for more than 20 years. As an IRS-authorized E-file provider and experienced tax professional, I’ve completed thousands of returns for individuals, businesses, partnerships, nonprofits, corporations, estates, and trusts. I take pride in breaking down complicated tax rules so clients actually understand what’s happening with their money.

My philosophy is simple:

more knowledge = less taxes.

What's new for Tax Year 2025?

I. Big Tax Picture – What Changed for 2025?

- Tax Cuts & Jobs Act didn’t die in 2025

- The One Big Beautiful Bill Act (OBBBA), signed July 4, 2025, made most of the 2017 Tax Cuts and Jobs Act individual and small-business rules permanent (7 brackets, doubled standard deduction, no personal exemptions, 20% QBI deduction, etc.).

- Standard deduction jumped again

- Base standard deduction for 2025 is now:

- $31,500 MFJ

- $15,750 Single/MFS

- $23,625 HOH

- Base standard deduction for 2025 is now:

- New deductions for seniors, tips, overtime, and car loan interest

- Extra $6,000 senior deduction per person 65+ (up to $12,000 MFJ) with income phase-outs.

- New above-the-line deductions for tips and overtime pay (2025–2028

- New above-the-line deduction for car loan interest on qualifying vehicles (2025–2028).

- Child Tax Credit (CTC) bumped and made more permanent

- CTC increased from $2,000 to $2,200 per qualifying child starting 2025, indexed for inflation from 2026 on; refundable portion also increased.

- SALT (State and local tax) cap temporarily raised

- SALT deduction cap jumps from $10,000 to $40,000 per return (with income-based phase-outs), for 2025–2029.

- Big capital cost goodies for businesses

- 100% bonus depreciation is restored and made permanent; Section 179 limits jump; new 100% write-off for certain U.S. “qualified production property.”

7. New “Trump Accounts” / 530A child accounts

- New tax-favored accounts for children, with tax-deferred growth and automatic account creation for many newborns, starting 2025–2026.

II. 2025 Standard Deduction, Brackets & Retirement Limits

A. Standard Deduction – 2025 (after OBBB)

For tax year 2025:

- Single / MFS: $15,750

- Married Filing Joint / Surviving Spouse: $31,500

- Head of Household: $23,625

Additional amounts (stacked on top):

- Existing age/blind add-ons (unchanged structure, indexed):

- About $2,000 per 65+ or blind single/HOH taxpayer; slightly lower per MFJ spouse.

- New senior bonus deduction (2025–2028, OBBB):

- Extra $6,000 per person 65+ (so up to $12,000 MFJ if both spouses ≥ 65).

- Phases out for MAGI over $75,000 single / $150,000 MFJ, fully gone by roughly $175k / $250k.

Example:

A married couple, both 67, with $120,000 AGI and no itemized deductions:

- Base standard deduction: $31,500

- Regular age-65 add-ons (approx.): $3,200 total

- New senior bonus: $12,000

Total deduction ≈ $46,700 – meaning only about $73,300 of their $120k is taxed.

B. 2025 Federal Income-Tax Brackets

- Still 7 brackets: 10%, 12%, 22%, 24%, 32%, 35%, 37%.

- OBBB makes these rates and the TCJA-style thresholds permanent, instead of expiring after 2025.

- All thresholds are inflation-adjusted annually via Rev. Proc. 2024-40 for 2025; details are in tables but not changed structurally.

C. Retirement Plan Contribution Limits (2025)

From IRS inflation releases:

- 401(k), 403(b), most 457:

- Employee elective deferral: $23,500

- Catch-up (50+): unchanged at $7,500 (so max $31,000 if 50+).

- Special catch-up age 60-63: $11,250

- Traditional & Roth IRAs:

- Contribution limit: $7,000; catch-up $1,000 (unchanged).

- FSAs / HSAs / HDHPs (2025 inflation):

- Health FSA salary reduction max: $3,300, carryover cap $660.

- HDHP and HSA thresholds are modestly higher; exact figures matter in plan documents, but concept is unchanged.

III. Major OBBB Individual Provisions Effective in 2025

A. Child Tax Credit (CTC) and Family-Focused Changes

- CTC increase & indexing

- Maximum CTC = $2,200 per qualifying child under 17 for 2025 (up from $2,000).

- Credit is indexed to inflation starting 2026.

- Income phase-outs still start at $200,000 single / $400,000 MFJ.

- Refundable portion (Additional CTC) increases up to $1,700 per child depending on earned income; minimum earned-income threshold remains $2,500.

Example:

MFJ with 2 kids under 17 and $60,000 AGI:

- Old max: $4,000

- New max: $4,400

That extra $400 directly cuts their tax bill.

- Other dependent & adoption credits

- $500 “Other Dependent Credit” (ODC) for older kids, elderly parents, etc., made permanent; previously scheduled to sunset with other TCJA items.

- Adoption credit:

- 2025 base limit around $17,280–$17,670 per child (inflation-adjusted).

- OBBB makes up to $5,000 of the adoption credit refundable, subject to income limits

- Recognizes tribal governments when determining “special needs” status.

- 529 plans & Trump Accounts

- OBBB expands some eligible expenses for 529 plans (more career and technical programs; details in IRS guidance).

- Trump Accounts / Section 530A / “530A accounts”:

- New tax-favored custodial accounts, tax-deferred growth similar to IRAs.

- Created under IRC §530A; targeted to children (generally U.S. citizen newborns in 2025–2029) with accounts often auto-opened when a Social Security number is issued.

- Contributions can come from parents, employers, and philanthropies, within annual caps; withdrawals are restricted and subject to tax if used for non-qualified purposes (similar to retirement accounts).

If you’ve got or are expecting a baby in the next few years, there’s now a government-blessed investment account that starts for them at birth.

B. New Deductions for Work Income – Tips, Overtime, and Seniors

- No Tax on Tips (2025–2028)

Structurally it’s not truly “no tax”—it’s an above-the-line deduction for “qualified tips”:

- Up to $25,000 of qualified tip income per year can be deducted from federal taxable income (2025–2028).

- Available whether a taxpayer itemizes or takes the standard deduction.

- Applies to occupations where tipping is “customary,” as defined by IRS guidance (restaurant servers, bartenders, hairstylists, etc.).

- Phases out as income rises (roughly MAGI over $150k single / $300k MFJ, with higher hard caps in some analyses).

- Still subject to Social Security, Medicare, and state taxes.

Example (server):

- W-2 wages: $40,000 (incl. $15,000 in reported tips)

- They can deduct $15,000 of tips above the line.

- Their taxable income drops by $15,000, potentially saving 12–24% of that amount in federal tax.

- No Tax on Overtime (2025–2028)

- Deduction covers only the overtime “premium” (the extra 0.5× over base rate under FLSA).

- Cap: typically, $12,500 per person / $25,000 MFJ of qualifying overtime premium per year.

- Income limit: generally, no deduction if MAGI > $150k single / $300k MFJ.

- Applies for tax years 2025–2028, retroactive to overtime earned starting Jan. 1, 2025.

Example (hourly worker):

- Base rate $20/hr, worked 200 overtime hours:

- Normal pay: 200 × $20 = $4,000

- Overtime premium (extra 0.5×): 200 × $10 = $2,000

- That $2,000 premium may be deductible above the line, lowering taxable income.

- Extra Senior Deduction (recap)

- New $6,000 deduction per 65+ taxpayer (2025–2028) on top of:

- Base standard deduction

- Existing age/blind add-ons

- Or on top of itemized deductions instead of the base standard deduction.

- New $6,000 deduction per 65+ taxpayer (2025–2028) on top of:

Planning angle: “If you’re 65+ and in the phase-out band, you may want to manage income (Roth conversions, capital gains harvesting, etc.) around those thresholds.”

C. Car Loan Interest Deduction (2025–2028)

- New above-the-line deduction for car loan interest

- Up to $10,000 per year of interest on a qualified passenger vehicle loan (car, SUV, light truck, motorcycle under 14,000 lbs GVWR) with final assembly in the U.S.

- Applies to loans starting after Dec. 31, 2024 and before Jan. 1, 2029.

- You don’t have to itemize to claim it; it reduces AGI directly.

Example:

- You finance a new U.S.-assembled SUV in 2025; annual interest is $4,000.

- You can deduct that $4,000 above the line (subject to detailed rules), even if you use the standard deduction.

- Reporting & lender issues

- New 2025 reporting rules for lenders; IRS granted penalty relief for 2025 while systems catch up.

D. SALT Cap Increase (2025–2029)

- Higher cap

- SALT deduction cap increased from $10,000 to $40,000 (or $20,000 MFS) for 2025–2029.

- For incomes above roughly $500,000 (single/MFJ thresholds differ), the cap phases down but never below $10,000.

- Practical impact

- Many upper-middle-income homeowners in high-tax states will itemize again, instead of using the standard deduction.

- Classic “bunching” strategies come back into play: prepay property taxes, accelerate state estimates, etc., in years where you’ll benefit from the higher cap.

E. 1099-K Threshold & ERC Clamp-Down

- 1099-K threshold reset

- OBBB restores the old $20,000 / 200-transactions threshold for Form 1099-K, undoing the ARPA $600 rule.

- Effective retroactively, with FAQs and transition relief.

- Employee Retention Credit (ERC) limitation

- OBBB limits credits and refunds for ERC claims for Q3 & Q4 2021 filed after Jan. 31, 2024.

- IRS released FAQs and is aggressively auditing questionable ERC claims.

If you’ve been pitched a late ERC claim, the window is effectively closed, and IRS scrutiny is high.

IV. Key Small-Business & Investor Changes for 2025

A. Depreciation & Expensing

- 100% bonus depreciation restored and made permanent

- OBBB permanently restores 100% bonus depreciation under §168(k) for qualifying property placed in service after enactment; ends the scheduled phase-down.

- New §168(n) – 100% for “qualified production property” (QPP)

- Extra 100% deduction for U.S. manufacturing / production property (think domestic factories and certain equipment), with special rules and elections.

- Expanded Section 179 expensing

- For tax years beginning in 2025:

- Max §179 deduction = $2,500,000

- Phase-out starts around $4,000,000 of qualifying purchases (fully phased out by about $6.5M).

- For tax years beginning in 2025:

If you’re a small or mid-size business, you can often write off most or all equipment purchases in year one; I just need to pick the best combination of §179 vs bonus vs regular MACRS for your situation.

B. QBI, Excess Business Losses & Other Pass-Through Rules

- QBI minimums (start 2026, enacted 2025)

- OBBB adds a new §199A(i):

- Requires at least $1,000 of qualified business income to claim the 20% QBI deduction.

- Has a minimum deduction of $400; both numbers indexed after 2026.

- These apply to tax years beginning after 12/31/2025, but they’re 2025 law changes—worth flagging now.

- OBBB adds a new §199A(i):

- Excess business loss (EBL) limitation made permanent

- The §461(l) EBL limitation (about $626,000 MFJ for 2025) is no longer scheduled to sunset; disallowed losses convert to NOLs in the next year.

C. Clean Energy & Other Sector-Specific Items (High-Level Only)

For most individual clients, you just need to know:

- Some home energy credits (25C, 25D, 25E, 30C, 45L, 45W, 179D) are scaled back or changed starting late 2025/2026.

- Several IRA-era green incentives are repealed or narrowed, especially for large projects; details matter mainly to developers and higher-dollar installations.

Message to homeowners: “If you’re doing energy upgrades, 2025 is still generally favorable, but the rules are shifting—bring your receipts; I’ll run the numbers under the new guidance.”

V. Other Notable 2025 Changes & Clarifications

A. AMT, EITC & Miscellaneous Indexed Items

- AMT exemption amounts for 2025 are higher again (roughly $137,000 MFJ; $88,100 single/HOH; $68,500 MFS).

- EITC, Saver’s Credit, education credits, and numerous thresholds (e.g., education-loan interest phaseouts) all got the usual inflation tweaks—no major structural overhaul for 2025.

B. Opportunity Zones in Rural Areas

- OBBB reduces the “substantial improvement” threshold from 100% to 50% of basis for property in qualified rural Opportunity Zones—important for rural development projects.

C. IRS Guidance & Transitional Relief

- 2025 sees penalty relief for:

- New information reporting on tips and overtime.

- New reporting of car loan interest by lenders.

- IRS updated withholding guidance and Publication 505 for 2025 to reflect the new standard deduction, CTC, and tip/overtime rules.

VI. Planning Angles for 2025

- If you’re 65+

- Make sure we claim all three layers:

- Base standard deduction

- Existing age/blind add-on

- New $6,000 senior deduction (if under income limits)

- Consider managing Roth conversions, RMD timing, and gains to stay under the senior deduction phase-out thresholds.

- Make sure we claim all three layers:

- If you earn tips or a lot of overtime (service, hospitality, trades)

- Track tips and overtime separately:

- We can often deduct up to $25k of tips and up to $12.5k/$25k of overtime premium (subject to income limits) above the line.

- Keep good records; W-2s and payroll systems won’t fully separate this yet.

- Track tips and overtime separately:

- If you have kids

- Expect a slightly bigger Child Tax Credit ($2,200 per child) and potentially higher refunds via the Additional CTC.

- For new or expected children, consider:

- Trump Accounts as a long-term savings vehicle.

- Coordination with 529s and updated adoption credit rules where applicable.

- If you’re a homeowner in a high-tax state

- With the SALT cap at $40,000, many clients should re-evaluate itemizing vs standard.

- Consider:

- Prepaying 2026 property taxes in late 2025 if within the higher cap and you’ll itemize this year.

- Bundling charitable giving in 2025 versus 2026 depending on itemizing expectations and upcoming new non-itemizer charitable deduction rules (those kick in 2026).

- If you run a business or own rentals

- Plan purchases of equipment, vehicles, and production assets to maximize 100% bonus and §179—but be smart about AMT and state rules.

- For losses:

- Understand that excess business loss limits are permanent; huge losses may not fully offset other income in a single year and will roll as NOLs.

- For 2026 and later:

- Check whether your QBI will meet the new $1,000 minimum and how the new rules impact your pass-through structure.

VII. What This Outline Does Not Cover

This summary focuses on federal individual and small-business income-tax changes for 2025 that are most likely to affect households, small businesses, and real-estate investors. It does not comprehensively cover:

- Large-corporate, international, or sector-specific provisions

- Non-tax spending cuts (Medicaid, SNAP, etc.)

- State and local tax law changes

All rules are current as of December 1, 2025, and may be modified by later IRS guidance or additional legislation.

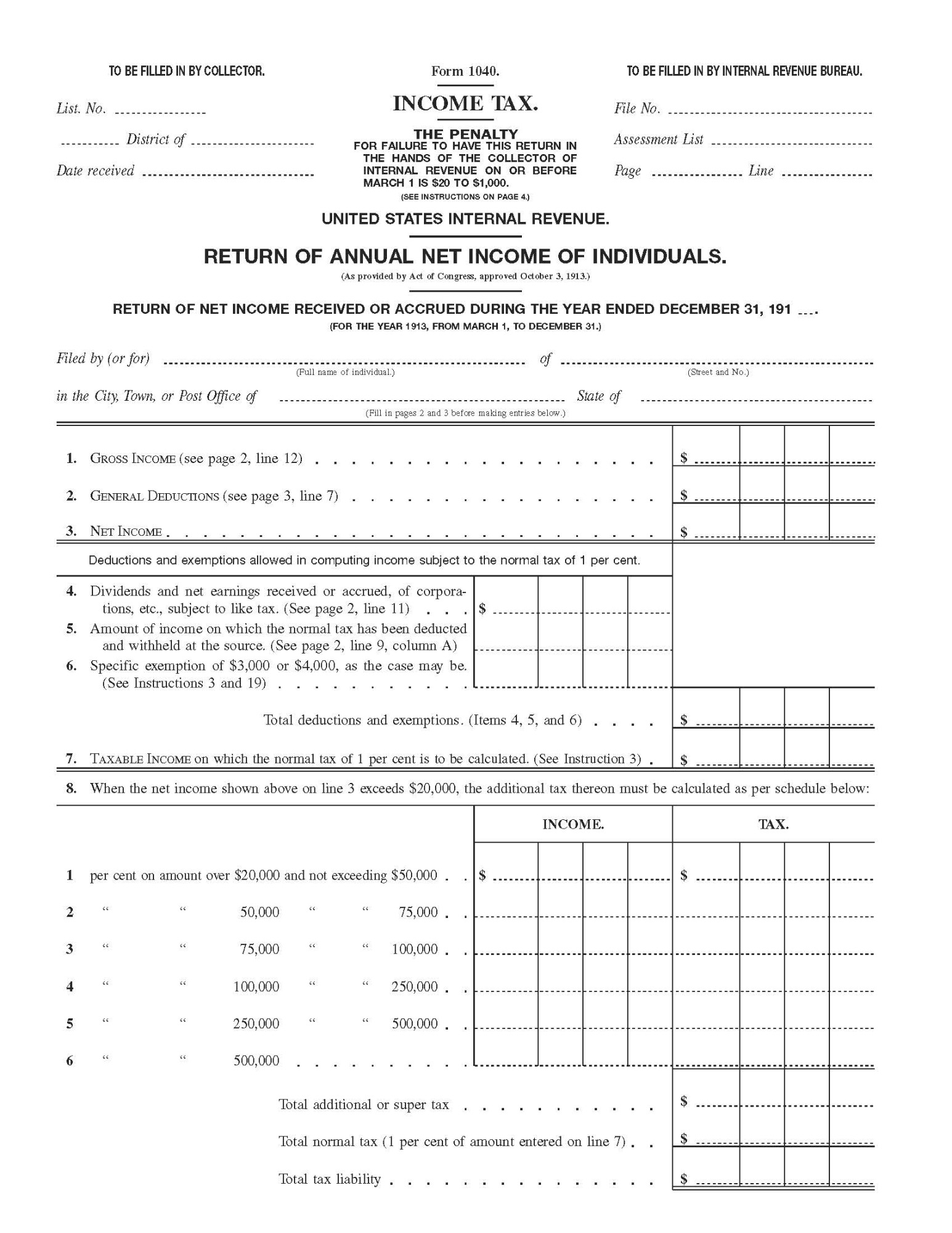

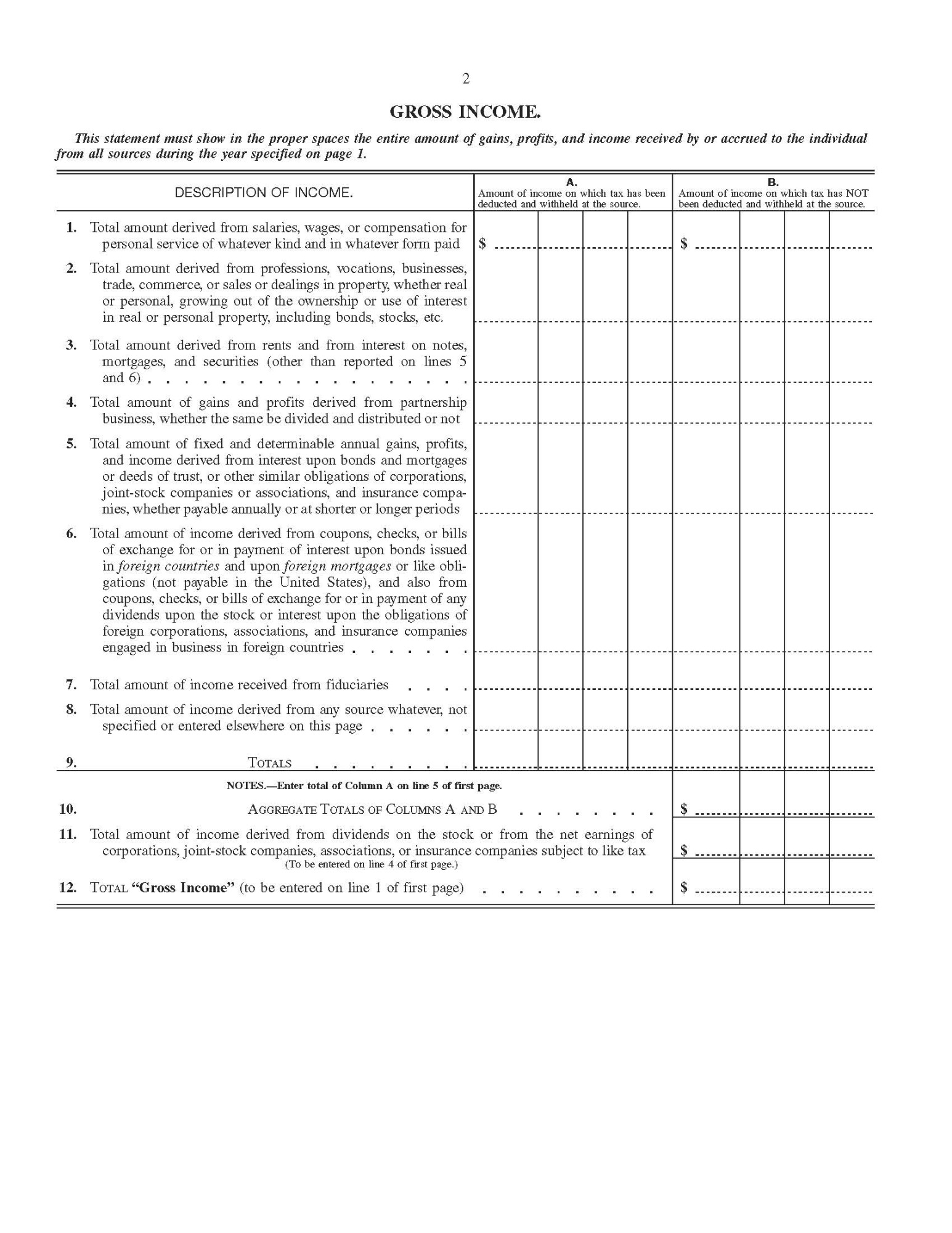

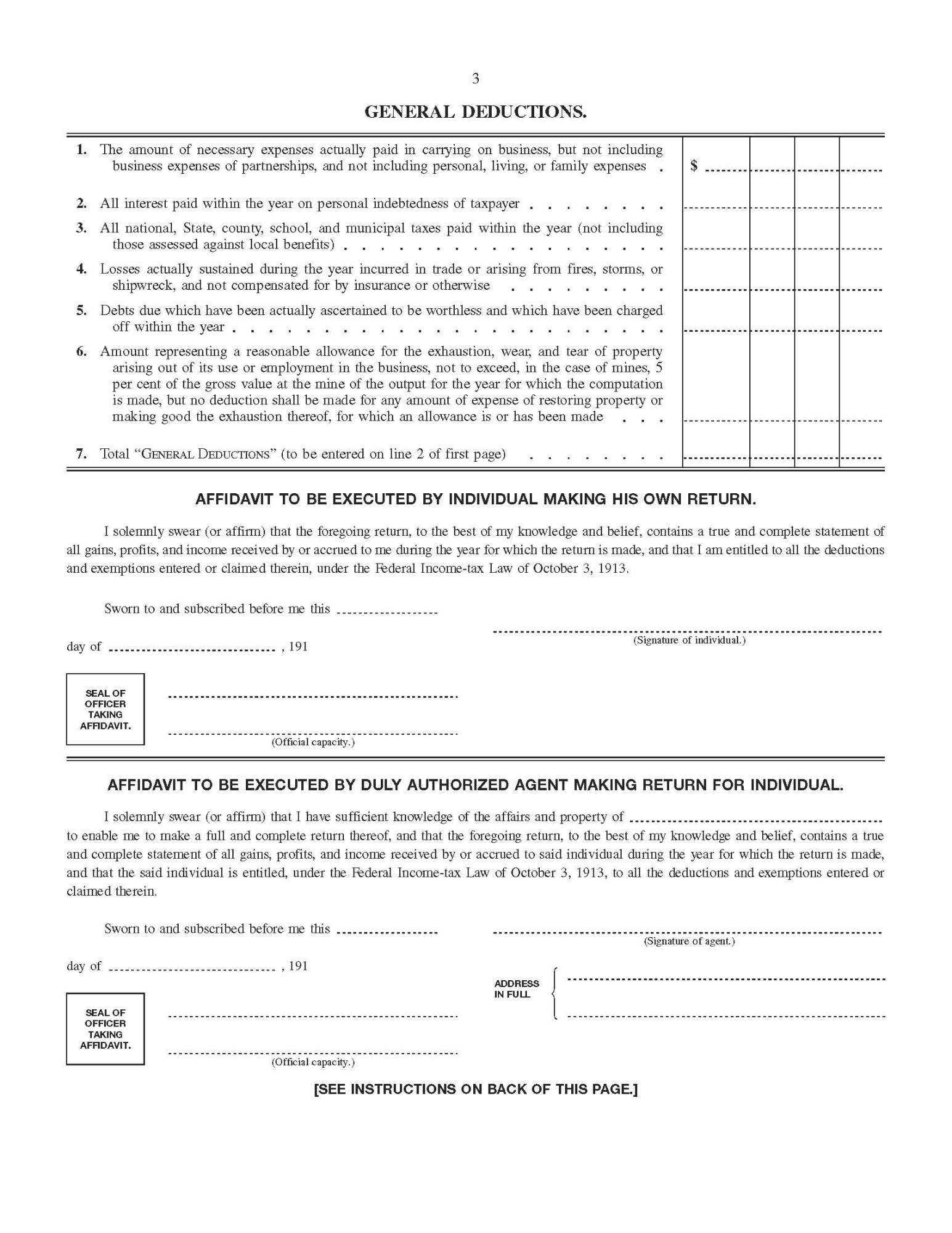

The First Form 1040 - 1913

This is the original Form 1040, first introduced in 1913. The entire return—including instructions—

was just four pages long and was used for both

individual and business income. Fast forward to today, and the tax code has

grown into a maze of more than 800 forms and schedules.

Same goal, very different level of complexity.

Times have definitely changed—taxes didn’t get simpler, they got a filing cabinet.